Executive Condominiums in Singapore: Understanding Eligibility, Financials, and Long-Term Benefits

Embarking on the journey to own an Executive Condominium (EC) in Singapore is an exciting venture. ECs, a unique blend of public and private housing, offer the comforts and amenities of a private condo at a more accessible price point. Introduced in 1995, they cater to the ‘sandwich’ class – those who exceed the income ceiling for public housing but find private properties a stretch.

Understanding the eligibility criteria for purchasing an EC is crucial. These rules, encompassing age, citizenship, income, and property ownership history, are designed to ensure ECs serve their intended demographic. Knowing these criteria is not just about legal compliance; it’s about aligning your aspirations with practical realities. It helps in financial planning, determining eligibility for grants, and avoiding future complications.

Table of Contents

Understanding Executive Condominiums

Foreign Ownership of Commercial Property in Singapore

An Executive Condominium (EC) in Singapore is a unique type of housing that caters to a specific segment of the population. It’s a form of housing introduced by the Singapore government in 1995, aimed at bridging the gap between public housing (like HDB flats) and private condominiums. ECs are developed and sold by private developers, but they come with certain restrictions and eligibility criteria, similar to public housing, especially in the initial years after their launch.

The Public-Private Hybrid Nature of ECs

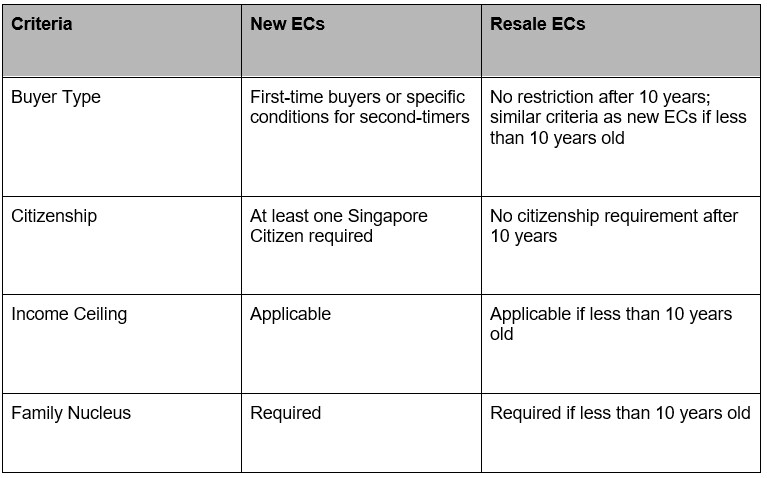

ECs are often described as a hybrid between public and private housing. For the first ten years after their construction, they are governed by rules similar to HDB flats. This means they are subject to regulations like the Minimum Occupation Period (MOP), during which the owner cannot sell the property on the open market. However, after this 10-year period, ECs ‘privatise’ and become akin to private condominiums. This transition allows them to be sold in the open market to both local and foreign buyers, which significantly increases their value and appeal.

Benefits of Choosing an EC

Choosing an EC comes with several benefits, making them a highly sought-after option for many Singaporeans:

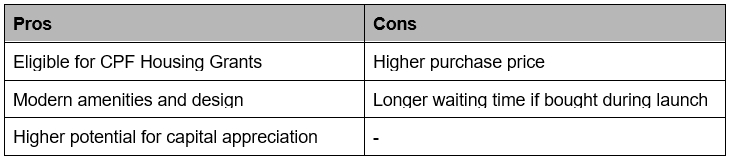

Affordability: ECs are priced lower than private condominiums, making them an attractive option for those who find private properties beyond their budget. This affordability is partly due to government subsidies.

Amenities and Lifestyle: Despite their lower price, ECs offer a range of amenities similar to private condos, such as swimming pools, gyms, security features, and sometimes even tennis courts. This provides a comfortable and upscale living experience.

Investment Potential: The unique nature of ECs, transitioning from public to private housing, offers significant investment potential. After the 10-year mark, when they become fully privatised, their value often appreciates, making them a wise investment choice.

Eligibility for Grants: Buyers of new ECs may be eligible for CPF housing grants, similar to those available for HDB flats, which can further offset the cost of purchase.

Community Living: ECs often foster a strong sense of community. Since they start as public housing, residents are typically Singapore.

Basic Eligibility Criteria for Executive Condominiums

Age Requirements

To be eligible to purchase an Executive Condominium (EC) in Singapore, the primary applicant must be at least 21 years old. However, if you’re applying under the Joint Singles Scheme, where two single individuals buy an EC together, both applicants need to be at least 35 years old. This age requirement ensures that buyers are typically in a stable phase of their careers, potentially making them more financially secure for such a significant investment.

Citizenship and Family Nucleus

A key criterion for EC eligibility revolves around citizenship and the composition of the family nucleus. The main applicant must be a Singapore Citizen, and at least one other applicant must be a Singapore Citizen or a Singapore Permanent Resident. This criterion is in place to prioritize the availability of ECs for Singaporeans.

The concept of a family nucleus is central to EC applications. You can apply as a family unit, which includes your spouse and children, if any; your parents and siblings; or your children under your legal custody (if you’re widowed or divorced). For joint singles, both applicants must be single (unmarried, divorced, or widowed).

First-Time Buyer Status

Being a first-time buyer is another crucial criterion. This means you and/or your spouse should not have previously owned or disposed of any property, whether locally or overseas, and should not have received any form of housing subsidy from HDB. This includes not owning or having disposed of any HDB flat bought from HDB, an EC/DBSS flat from a developer, or a resale HDB flat with a CPF Housing Grant.

Income Ceiling for EC Buyers

The income ceiling for EC buyers is another important factor. As of my last update, the total gross monthly household income must not exceed SGD 16,000. This ceiling is reviewed periodically to ensure that ECs remain accessible to the target group they are meant for. The income ceiling is a balancing act to ensure affordability while maintaining the exclusivity and quality of ECs.

Detailed Eligibility Conditions for Executive Condominiums

HDB Eligibility Schemes

When applying for an Executive Condominium (EC), applicants must qualify under one of the Housing & Development Board (HDB) eligibility schemes. These schemes are designed to cater to different family units and social circumstances.

1. Public Scheme:

The Public Scheme is for those applying with their family nucleus. This includes spouses and children, parents and siblings, or children under your legal custody (applicable for widowed or divorced applicants).

It’s designed to encourage family living, ensuring that ECs are used as family homes.

2. Fiancé/Fiancée Scheme:

This scheme is for couples who are engaged to be married.

It allows couples to plan for their future together, securing a home before their marriage.

Under this scheme, couples need to submit their marriage certificate to HDB within three months of taking possession of the EC.

3. Joint Singles Scheme:

For single individuals who are at least 35 years old, the Joint Singles Scheme allows two such individuals to apply for an EC together.

This scheme is particularly beneficial for singles who prefer to co-own a property with a friend or sibling, offering them a chance to invest in an EC.

4. Orphans Scheme:

The Orphans Scheme is a thoughtful inclusion for applicants who are orphans and wish to buy an EC with their siblings.

To be eligible, applicants and their siblings must be single (unmarried, divorced, or widowed) and orphaned.

Property Ownership Rules

Understanding the property ownership rules is crucial when applying for an EC.

Restrictions on Owning Other Properties:

- Applicants must not own other property overseas or locally, or have not disposed of any within the last 30 months.

- This rule ensures that ECs are allocated to those who do not already own a home.

Previous Property Transactions:

- Applicants must not have bought a new HDB/DBSS flat or an EC, or received a CPF Housing Grant before.

- This condition is in place to prioritize housing allocation to first-time buyers or those who have not previously benefited from government housing subsidies.

Financial Considerations for Executive Condominiums

Understanding the Income Ceiling

The income ceiling for purchasing an Executive Condominium (EC) is a crucial financial consideration. As of my last update, the ceiling is set at SGD 16,000 for the total gross monthly household income. This means the combined monthly income of all persons listed in the application must not exceed this amount. It’s important to stay updated on this figure, as it is subject to change and can impact your eligibility.

Calculating Affordability and Loan Eligibility

Before diving into the EC market, it’s essential to assess your financial health. Calculating your affordability involves considering your monthly income, existing debts, and other financial commitments. Loan eligibility, on the other hand, will depend on factors like your credit score, age, and income stability. Banks and financial institutions use these to determine how much they’re willing to lend you.

Impact of Total Debt Servicing Ratio (TDSR) and Mortgage Servicing Ratio (MSR)

Two critical ratios come into play when applying for a loan to purchase an EC: the Total Debt Servicing Ratio (TDSR) and the Mortgage Servicing Ratio (MSR).

- TDSR: This is the portion of a borrower’s gross monthly income that goes towards servicing all debts, including the EC loan. As per regulations, your TDSR should not exceed 60%.

- MSR: This is specific to housing loans. The MSR limits the EC loan repayment to 30% of the borrower’s gross monthly income.

Understanding these ratios is vital as they determine your loan quantum and ensure that you don’t over-leverage financially.

Downpayment and Loan Quantum for ECs

When purchasing an EC, you’ll need to make a downpayment, which is partly payable in cash and partly with your CPF savings. The exact amount will depend on the loan quantum – the total loan amount you’re eligible to borrow. Typically, you can borrow up to 75% of the EC’s purchase price or valuation, whichever is lower, meaning you’ll need to prepare at least 25% for the downpayment.

Additional Costs (Legal Fees, Buyer Stamp Duty, etc.)

Apart from the downpayment, there are additional costs to consider:

- Legal Fees: These are the costs of engaging a lawyer to handle the legal aspects of your property purchase.

- Buyer Stamp Duty (BSD): This is a tax paid on the purchase price or market value of the property, whichever is higher.

Other Miscellaneous Costs: These may include administrative fees, property agent fees (if applicable), and home insurance.

CPF Housing Grants for Executive Condominiums

Types of Grants Available

When purchasing an Executive Condominium (EC) in Singapore, potential buyers can tap into various Central Provident Fund (CPF) Housing Grants. These grants are designed to make ECs more affordable and accessible. The two main types of grants available for EC buyers are the Family Grant and the Half-Housing Grant.

Family Grant

The Family Grant is aimed at couples or families who are purchasing an EC. The eligibility for this grant depends on your combined income and whether you are a first-time applicant. The grant amount can significantly subsidize the cost of the EC, making it a more viable option for families looking to upgrade their living situation.

Half-Housing Grant

The Half-Housing Grant is designed for those who are not first-time applicants but are buying an EC with a spouse who is a first-time applicant. This grant acknowledges the mixed status of the applicants and still provides some level of subsidy, albeit at a reduced amount compared to the Family Grant.

Eligibility for CPF Housing Grants

To be eligible for these grants, applicants must meet certain criteria:

- Citizenship: At least one applicant must be a Singapore Citizen.

- Income Ceiling: Your combined monthly household income must not exceed the stipulated limit.

First-Time Buyer Status: For the Family Grant, both applicants must be first-time buyers. For the Half-Housing Grant, one applicant must be a first-time buyer.

Grant Amounts Based on Income Levels

The amount of grant you are eligible for depends on your combined household income. The lower the income, the higher the grant amount, as the scheme is designed to provide more substantial assistance to lower-income families. It’s important to check the latest updates on grant amounts and income ceilings, as these figures are subject to periodic revisions by the authorities.

Special Considerations for Executive Condominiums

Buying EC as a Single Applicant

While Executive Condominiums (ECs) are primarily targeted at couples and families, single applicants are not entirely excluded. If you’re a single Singaporean, you can apply for an EC under the Joint Singles Scheme, provided you are at least 35 years old. This scheme allows two or more single individuals to come together to purchase an EC. It’s a fantastic opportunity for singles who wish to invest in a property that offers the benefits of an EC, such as lifestyle amenities and the potential for capital appreciation.

Resale Levy for Second-Time Buyers

If you’re a second-time buyer looking to purchase an EC, it’s important to be aware of the resale levy. This levy is applicable if you have previously purchased a subsidized flat from the Housing & Development Board (HDB) or taken advantage of a CPF Housing Grant. The resale levy is a way of ensuring a fair distribution of subsidies among various groups of buyers. The amount varies depending on the type and size of the flat you previously owned and is payable upon the purchase of your EC. It’s crucial to factor in this cost when planning your finances for the EC purchase.

Minimum Occupation Period (MOP) Requirements

The Minimum Occupation Period (MOP) is a significant consideration for EC buyers. ECs, like HDB flats, come with an MOP of five years from the date of the Temporary Occupation Permit (TOP) or key collection. During this period, you are not allowed to sell the EC in the open market or rent out the entire unit. This rule is in place to ensure that ECs are used primarily for owner-occupation and not for short-term investment or rental purposes. After the MOP, you are free to sell the EC to Singapore Citizens or Permanent Residents. After 10 years, the EC becomes fully privatized, and you can sell it to anyone, including foreigners.

Comparing New and Resale Executive Condominiums

When venturing into the Executive Condominium (EC) market in Singapore, one of the key decisions you’ll face is choosing between a new EC and a resale EC. Both options have their unique sets of eligibility criteria, financial implications, and pros and cons.

Differences in Eligibility Criteria

Financial Implications

Pros and Cons of Each Option

New ECs

Resale ECs

Long-Term Considerations for Executive Condominiums

When considering an Executive Condominium (EC) purchase in Singapore, it’s not just the immediate benefits and costs that matter. Long-term considerations play a crucial role in ensuring that your investment not only meets your current needs but also contributes positively to your future financial health.

Investment Potential of ECs

ECs are often viewed as a smart investment choice in Singapore’s real estate market. Their unique position as a hybrid between public and private housing gives them a distinctive edge:

- Initial Affordability: ECs are initially more affordable compared to private condominiums, thanks to government subsidies. This affordability factor makes them an attractive option for buyers looking for value for money.

- Capital Appreciation: Over time, ECs have shown a tendency for steady capital appreciation. Once they cross the 10-year mark and become fully privatized, their value often increases, aligning more closely with the prices of private condominiums.

The transition from Public to Private Property

One of the most significant aspects of ECs is their transition from public to private housing after 10 years. This transition brings several benefits:

- Increased Market Value: As ECs move into the private property bracket, they typically experience an increase in market value.

- Broader Selling Options: Post-privatization, ECs can be sold to foreigners, which broadens the potential buyer pool and can positively impact resale value.

Rental and Resale Opportunities

ECs also present lucrative rental and resale opportunities:

- Rental Potential: After the Minimum Occupation Period (MOP) of five years, owners can rent out their ECs. This can be a steady source of income, especially in areas with high demand for rental properties.

- Resale Prospects: The resale market for ECs is quite dynamic. Buyers who purchase ECs during the initial launch phase often find that their property’s value has appreciated by the time they are eligible to sell it (post-MOP). This appreciation makes ECs a viable option for those looking at real estate as a long-term investment.

Conclusion

As we wrap up our comprehensive guide on the eligibility criteria for buying an Executive Condominium (EC) in Singapore, it’s clear that while the journey to owning an EC can be intricate, it’s also filled with opportunities. From understanding the unique blend of public and private housing features of ECs, navigating through the various eligibility criteria and financial considerations, to exploring the long-term investment potential, each step is crucial in making an informed decision.

Remember, purchasing an EC is not just about finding a place to live; it’s about making a wise investment in your future. The blend of affordability, lifestyle amenities, and investment potential makes ECs a unique and attractive option in Singapore’s real estate market.

However, we understand that this journey, filled with various rules and considerations, can be daunting. That’s where our expertise comes in. Our team of dedicated real estate professionals is equipped with the knowledge and experience to guide you through every step of the process. Whether you’re a first-time buyer, a single applicant, or a second-time buyer considering an EC, we’re here to provide personalized advice and support.

Don’t let the complexities of the process deter you from your dream of owning an EC. Reach out to our real estate advisors today, and let us help you navigate this journey with ease and confidence. Together, we can turn your dream of owning an Executive Condominium into a reality.

🔗 Contact us now to start your journey towards owning the perfect Executive Condominium for you and your family. We’re here to make your journey smooth and successful!

Frequently Asked Questions (FAQs)

An EC is a type of housing in Singapore that blends public and private housing features. It’s built and sold by private developers but comes with eligibility restrictions similar to public housing.

Eligibility is generally for Singapore Citizens who are at least 21 years old (35 for singles under the Joint Singles Scheme), with an income ceiling of SGD 16,000 for the household. Other conditions like family nucleus requirements also apply.

Yes, singles aged 35 and above can purchase an EC under the Joint Singles Scheme, where two or more singles can apply together.

Yes, eligible buyers can apply for the Family Grant or Half-Housing Grant, depending on their circumstances.

The MOP for an EC is 5 years, during which the owner cannot sell the property in the open market or rent out the entire unit.

No, you must not own other property overseas or locally or have not disposed of any within the last 30 months to be eligible for an EC.

A new EC is purchased directly from a developer, while a resale EC is bought from an existing owner. Resale ECs are typically older but don’t have waiting times for construction.

Yes, if you have previously purchased a subsidized flat or received a CPF Housing Grant, you may be subject to a resale levy when buying an EC.

Foreigners cannot buy new ECs or those less than 10 years old. However, once an EC is over 10 years old and fully privatized, it can be sold to anyone, including foreigners.

The TDSR limits the amount you can spend on monthly debt repayments to 60% of your gross monthly income, affecting the loan amount you can secure for purchasing an EC.